Unlock financial success through the 50/30/20 rule. Learn to manage your finances effectively, achieve your goals, and secure your future

Introduction

In the journey to financial success, managing your income wisely is crucial. One popular and effective method that helps individuals take control of their finances is the 50/30/20 rule. This rule offers a straightforward yet powerful way to allocate your income, ensuring that you meet your needs, enjoy some wants, and save for the future. In this article, we will explore the 50/30/20 rule in detail, understand how it works, and discuss its advantages, challenges, and real-life applications. By the end, you’ll be equipped with the knowledge to steer your financial ship towards success.

Key Takeaways:

- The 50/30/20 rule recommends allocating 50% of your after-tax income to cover essential needs and obligations.

- The remaining half of your income should be divided into 20% for savings and debt repayment and 30% for discretionary expenses.

- This rule serves as a financial guideline designed to assist individuals in managing their finances, prioritizing savings for emergencies and retirement.

- The primary aim of the 50/30/20 ruleex is to strike a balance between meeting essential needs and proactively saving for the future, particularly for retirement.

- Simplify adherence to the 50/30/20 rule by automating deposits, setting up automatic bill payments, and monitoring income fluctuations.

What is 50/30/20 Rule

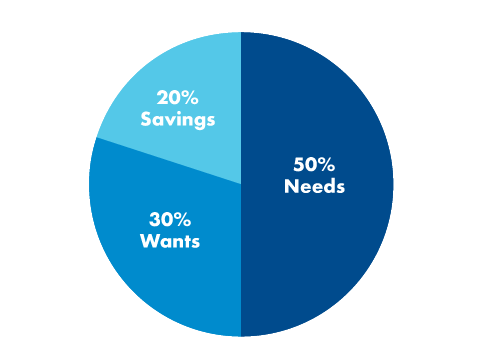

The 50/30/20 rule, also known as the 50/30/20 budget, is a simple guideline for managing your finances. It suggests dividing your after-tax income into three categories:

Needs (50%):

This category includes essential expenses, such as housing, utilities, groceries, transportation, and insurance. These are the things you can’t do without. Properly allocating this portion ensures you cover the necessities that maintain your daily life.

Examples of “needs” include but are not limited to:

- Rent or mortgage payments: The cost of housing, whether you own or rent a property, is a fundamental need.

- Car payments: If you rely on a vehicle for transportation, monthly car payments are considered a necessity.

- Groceries: Purchasing food and essential household items to sustain yourself and your family is a basic need.

- Insurance and health care: Health insurance, along with insurance for other essential aspects of life, falls under the “needs” category, as does necessary healthcare expenses.

- Minimum debt payments: These are payments required to meet your financial obligations and avoid defaulting on loans and credit cards.

- Utilities: Covering the costs of utilities such as electricity, gas, water, and internet is vital for daily living and is thus categorized as a “need.”

Wants (30%):

Wants are non-essential expenses, such as dining out, entertainment, shopping for clothes or gadgets, and hobbies. These expenses add enjoyment to your life but aren’t necessities. The “wants” category is designed to provide you with financial flexibility to enjoy life beyond the essentials.

In general, examples of “wants” include but are not limited to:

- New unnecessary clothes or accessories like handbags or jewelry: Fashion items and accessories that are not essential for daily life or work.

- Tickets to sporting events: Attending games or events for entertainment rather than necessity.

- Vacations or other non-essential travel: Traveling for leisure and non-essential purposes, such as vacations.

- The latest electronic gadget (especially an upgrade over a fully functioning prior model): Purchasing new electronics or gadgets when your current ones are still functional.

- Ultra-high-speed Internet beyond your streaming needs: Opting for extremely fast internet speeds beyond what is necessary for basic online activities, like streaming or working from home.

Savings and Debt Repayment (20%):

The final 20% of your income is dedicated to securing your financial future. It includes saving for emergencies, retirement, and paying off debts. This portion acts as a safety net and a means to work towards a debt-free life, ultimately providing financial peace of mind.

Examples of savings could include:

- Creating an emergency fund: Setting aside a portion of your income to build a financial cushion for unexpected expenses, like medical bills or car repairs.

- Making IRA contributions to a mutual fund account: Saving for retirement by contributing to an Individual Retirement Account (IRA), which may include investments in mutual funds.

- Investing in the stock market: Allocating funds to invest in stocks or other securities to grow your wealth over time.

- Setting aside funds to buy physical property for long-term holding: Saving for the purchase of real estate or physical assets that can appreciate in value, such as a home or rental property.

- Making debt repayments beyond minimum payments: Paying off debts more aggressively than the minimum required payments to reduce the overall debt burden and save on interest costs.

The Importance of Budgeting

Before diving into how to implement the 50/30/20 rule, it’s essential to stress the significance of budgeting. A budget is like a roadmap for your financial journey. It helps you keep track of where your money is going and ensures that you stay on the right path. By following a budget, you can avoid overspending and make sure you allocate the necessary funds for each category. Budgeting acts as a guiding tool that empowers you to manage your finances effectively.

Implementing the 50/30/20 Rule

Now, let’s break down the steps to implement the 50/30/20 rule effectively.

Step 1: Calculate Your Monthly Income

Start by determining your after-tax monthly income. This is the money you actually receive in your bank account after taxes are deducted. Your income should be consistent, so you can base your budget on it. Knowing your income is the foundational step towards building your financial plan.

Step 2: Determine Your Needs (50%)

The first category, “Needs,” should account for 50% of your income. Calculate this amount and allocate it to essential expenses. Make a list of your necessities, such as rent or mortgage, utilities, groceries, transportation, and insurance premiums. This 50% should cover all these expenses. Properly allocating your needs ensures you can maintain a stable and secure lifestyle.

Step 3: Identifying Wants (30%)

Your wants category should account for 30% of your income. Here, you can allocate funds for dining out, entertainment, shopping for non-essential items, and hobbies. While it’s essential to enjoy life, this category should not exceed 30% to maintain financial balance. Allocating 30% to wants gives you the financial freedom to enjoy your life without overspending.

Step 4: Allocating to Savings and Debt Repayment (20%)

The final 20% of your income is for securing your financial future. This includes saving for emergencies, retirement, and paying off debts. Allocate this portion diligently, as it will help you achieve financial stability and freedom. Proper allocation to savings and debt repayment lays the foundation for your long-term financial well-being.

The Advantages of the 50/30/20 Rule

The 50/30/20 rule offers several advantages:

- Simplicity: This rule is easy to understand and implement, making it accessible to everyone. Its simplicity makes it a practical choice for those new to budgeting.

- Balance: It ensures a balance between your current needs and future goals, promoting financial well-being. Balancing your financial priorities is key to achieving financial success.

- Savings: By allocating 20% to savings and debt repayment, you build a financial safety net and work towards a debt-free life. This sets you on the path to financial security.

- Financial Awareness: Following the rule forces you to pay attention to your expenses and make informed decisions. It fosters financial mindfulness and responsibility.

Common Challenges and How to Overcome Them

While the 50/30/20 rule is effective, it’s not without challenges. One common issue is overspending in the “Wants” category. To overcome this, consider tracking your expenses, creating a separate “wants” budget, and practicing self-control when tempted to overspend. Addressing these challenges empowers you to stay on track and follow the rule effectively.

Real-Life Examples

Let’s explore some real-life scenarios to better understand how the 50/30/20 rule works:

Example 1 – Sarah: Sarah earns $4,000 per month after taxes. She spends $2,000 on her needs, $1,200 on her wants, and saves $800. This allocation aligns perfectly with the rule. Sarah’s financial allocation demonstrates the practicality and balance achievable through the 50/30/20 rule.

Example 2 – John and Lisa: John and Lisa, a couple with a combined monthly income of $7,500 after taxes, allocate $3,750 for their needs, $2,250 for their wants, and save $1,500, following the 50/30/20 rule effectively. John and Lisa’s financial allocation showcases how the rule can be adapted to fit the financial dynamics of a household.

Tips for Long-Term Financial Success

To ensure long-term financial success, consider the following tips:

- Review Your Budget Regularly: Life circumstances change, so your budget should adapt accordingly. Regular reviews ensure your financial plan remains relevant and effective.

- Automate Your Savings: Set up automatic transfers to your savings or retirement accounts to ensure consistent savings. Automation simplifies the savings process and fosters discipline.

- Emergency Fund: Prioritize building an emergency fund to cover unexpected expenses. An emergency fund acts as a financial safety net, providing security during unforeseen circumstances.

- Debt Repayment: Focus on paying off high-interest debts to free up more funds for savings and wants. Reducing debt creates more financial room for your other financial priorities.

- Invest Wisely: As your savings grow, consider investing to accelerate your wealth-building journey. Smart investments can help your money work for you and compound over time.

Adjusting the Rule to Your Needs

While the 50/30/20 rule is a great starting point, it’s not one-size-fits-all. You can adjust the percentages to better suit your situation. For instance, if you have higher financial responsibilities, you may allocate 60% to needs and reduce wants to 25%. The key is to maintain a balance that ensures your financial stability and future security. Adjusting the rule demonstrates its flexibility and adaptability to diverse financial scenarios.

Options Beyond the 50/30/20 Rule

The 50/30/20 rule may not suit everyone, and it’s valuable to explore various budgeting strategies to find what works best for you. Here are some alternative approaches:

- Zero-based budgeting: Under this method, you assign a specific purpose to every dollar you earn. This entails creating a more extensive list of categories than the three found in the 50/30/20 rule. Compile all your expenses, savings objectives, and debts, and allocate your entire post-tax income among these categories. This approach is most suitable for individuals comfortable with the meticulous record-keeping required and those with consistent monthly income.

- Envelope system: Another choice is to allocate a set amount of cash to designated envelopes for each spending category—and restrict your expenses to these predefined amounts. This method demands strong organizational skills but may not be practical for bills paid online or with credit cards. Additionally, it involves the risk of misplacing or theft of cash.

- Multiple-account budget: Utilize your bank accounts to streamline your budgeting. This involves setting up various accounts, which is especially convenient with online banks, for different expense categories, similar to the divisions in the 50/30/20 rule. Create regular transfers from your primary checking account to these subsidiary accounts to establish spending limits effortlessly.

- Pay-yourself-first budget: With this strategy, you arrange an automated transfer from your checking account to your savings account(s) immediately after receiving your income. This ensures that your long-term savings goals are covered, allowing you to spend the remainder of your earnings on necessities and desires without specifying precise allocations. As long as you avoid overdrawing your account, you’re on track.

Monitoring Your Progress

Regularly assess how well you are following the 50/30/20 rule. Tracking your expenses, reviewing your savings, and evaluating your debt reduction can help you stay on the path to financial success. Monitoring your progress ensures that you remain aligned with your financial goals and continue making positive strides towards financial stability.

Conclusion

In conclusion, the 50/30/20 rule provides a clear and simple framework for managing your income effectively. By allocating your funds to needs, wants, and savings, you can strike a balance that leads to financial stability and long-term success. Remember that this rule is flexible, and you can adjust it to fit your unique circumstances. With disciplined budgeting and a focus on your financial goals, you can achieve the financial success you desire. The 50/30/20 rule is a versatile tool that empowers you to take control of your financial journey and make informed financial decisions.

Frequently Asked Questions

Free Invoice Template for Excel: Streamline Your Billing Process

In the fast-paced world of business, efficiency and accuracy in billing are paramount. At SaveSaga,…

20+ Budget-Friendly Gift Ideas for Every Special Occasion

Unlock the secret to heartfelt gifting without breaking the bank. Explore our guide for creative,…

30+ Ways to Make $1000 Fast in 2024: Legal, Legit, and Lucrative

#MAKE MONEY Make $1000 fast Are you struggling to make ends meet? Do you need…

How to Create a Budget as a College Student, 13 best ways

In the whirlwind of college life, Budget as a College Students can be a daunting…

8 Proactive Strategies On How To Protect From Inflation For Financial Stability

Explore proactive budgeting and investment strategies on how to protect from inflation and to maintain…

Decoding Fixed And Variable Expenses: Achieving Financial Stability Through Smart Budgeting

Master the art of financial stability with our guide on budgeting. Explore the balance between…